What Is an Income Statement?

An income statement, also called a profit and loss (P&L) statement, summarizes your business’s financial performance over a set period—monthly, quarterly, or annually.

It answers three core questions:

- How much did the business earn?

- What did it cost to operate?

- How much profit (or loss) remains?

Unlike day-to-day bookkeeping, an income statement highlights trends that help guide planning, pricing, and spending decisions.

What Is an Income Statement Used For?

| Purpose | Why It Matters |

| Track revenue and expenses | Identify growth trends and rising costs |

| Support business decisions | Evaluate whether strategies are working |

| Attract investors or lenders | Present clear, organized financial results |

| Prepare tax returns | Ensure accurate income and expense reporting |

Main Components of an Income Statement

Income Statement at a Glance

| Component | What It Shows |

| Revenue | Total income earned |

| Cost of Goods Sold (COGS) | Direct costs to produce goods/services |

| Gross Profit | Revenue minus COGS |

| Operating Expenses | Day-to-day business costs |

| Operating Income | Profit from core operations |

| Non-Operating Items | Interest, taxes, asset losses |

| Net Income | Final profit or loss |

Revenue

Revenue represents all income earned during the reporting period, before expenses.

Common revenue sources include:

- Sales of products or services

- Interest income

- Rental income

- Royalties

Cost of Goods Sold (COGS)

COGS includes direct costs tied to producing or delivering what you sell.

| Typical COGS Items |

| Raw materials |

| Direct labor |

| Manufacturing or production overhead |

Gross Profit

Gross Profit = Revenue − COGS

This figure shows how much income is available to cover operating expenses and generate profit.

Operating Expenses

Operating expenses are indirect costs required to run the business.

| Operating Expense Examples |

| Salaries and wages |

| Rent and utilities |

| Marketing and advertising |

| Legal and accounting fees |

| Insurance and office supplies |

Operating Income

Operating income reflects profit from normal business operations, before taxes and interest.

Non-Operating Expenses

These expenses fall outside daily operations but still affect profitability:

- Interest on loans

- Asset sale losses

- Income taxes

Net Income

Net income is the bottom line—your total profit or loss after all expenses and taxes.

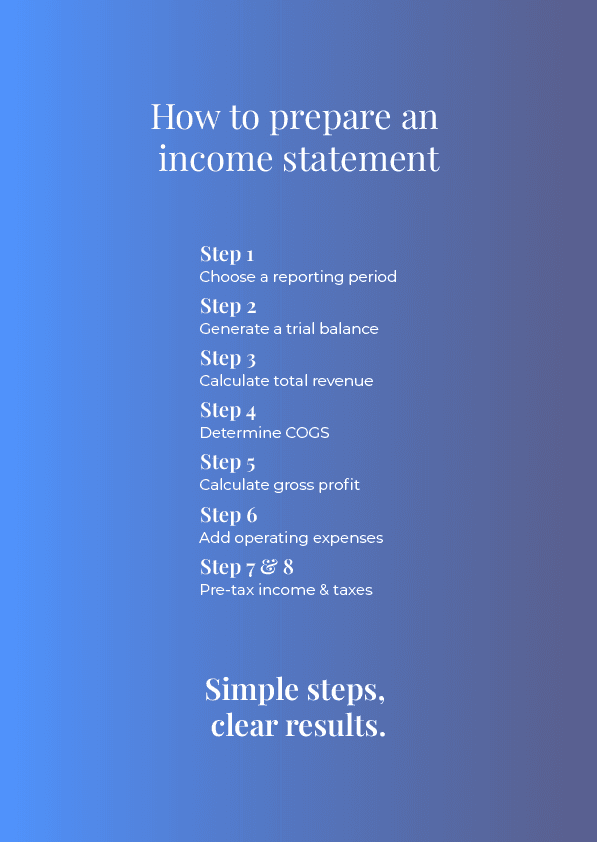

How to Prepare an Income Statement: 8 Simple Steps

Step-by-Step Overview

| Step | Action |

| 1 | Choose a reporting period |

| 2 | Generate a trial balance |

| 3 | Calculate total revenue |

| 4 | Determine COGS |

| 5 | Calculate gross profit |

| 6 | List operating expenses |

| 7 | Calculate operating income |

| 8 | Subtract taxes and interest |

Step 1: Choose a Reporting Period

Most businesses prepare income statements monthly, quarterly, or annually. Shorter periods help you adjust quickly, while longer periods show broader trends.

Step 2: Generate a Trial Balance

Use your accounting software to pull a trial balance for the selected period. This report provides the account balances used to build your income statement.

Step 3: Calculate Total Revenue

Add up all income earned during the period. If the statement covers a specific department or product line, include only related revenue.

Step 4: Determine Cost of Goods Sold

List all direct costs required to produce or deliver your goods or services.

Step 5: Calculate Gross Profit

Subtract COGS from total revenue to measure production profitability.

Step 6: Include Operating Expenses

Compile indirect costs such as rent, utilities, insurance, and professional fees.

Step 7: Calculate Operating Income

Subtract operating expenses from gross profit to see earnings from core operations.

Step 8: Account for Taxes and Interest

Subtract applicable income taxes and interest expenses to arrive at net income.

Tips for Creating Accurate Income Statements

Use Reliable Accounting Software

Tools like QuickBooks, Xero, or Zoho Books reduce errors and streamline reporting.

Maintain Consistent Records

Accurate, up-to-date records make income statements easier to prepare and review.

Work With a Professional

An accountant can help ensure accuracy, interpret results, and use income statements for planning—not just compliance.

Prepare Your Income Statement with SSL Associates

Knowing how to prepare an income statement helps you understand where your business stands and where it’s headed. It supports better decisions today and stronger planning for the future.

The team at SSL Associates can help you:

- Prepare accurate income statements

- Understand what your numbers are telling you

- Use financial reports to guide business growth