What Is the IRS Tax Filing Deadline?

The federal tax filing deadline is typically April 15th, unless it falls on a weekend or holiday. For the 2025 tax year, the deadline remains April 15th.

It’s important to know that the IRS treats filing your return and paying your taxes as separate requirements. Missing either deadline can result in penalties and interest.

What Happens If You File Taxes Late?

If You Are Due a Tax Refund

If the IRS owes you a refund, there is no penalty for filing late. However:

- The IRS does not issue refunds until a return is filed

- You have three years from the original deadline to claim your refund

- After three years, the refund is permanently forfeited

If You Owe Taxes

If you owe taxes and file late, the IRS applies penalties and interest until action is taken. Filing your return as soon as possible limits the damage.

IRS Penalties for Filing Taxes Late

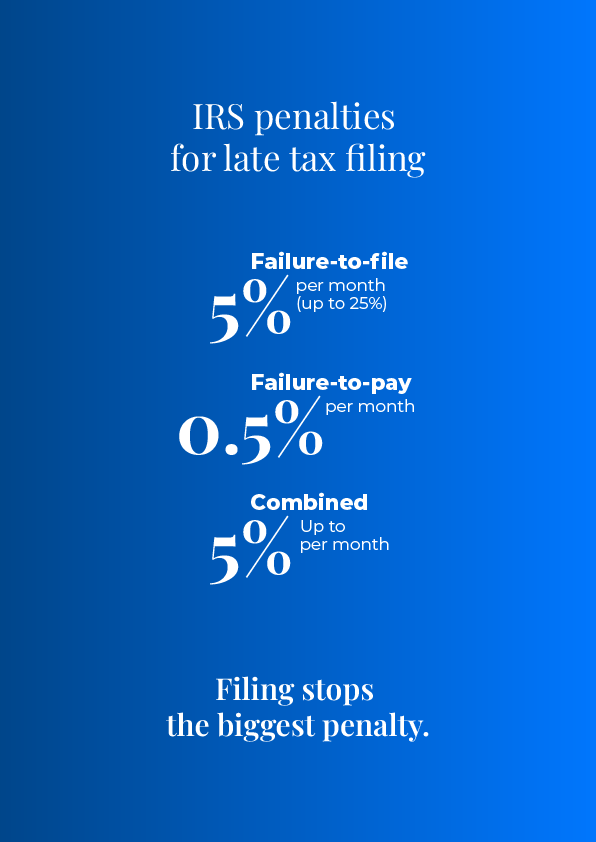

Failure-to-File Penalty

The failure-to-file penalty is the most severe IRS penalty for late tax returns.

- 5% of unpaid taxes per month

- Capped at 25% of the total tax owed

- Begins accruing the day after the filing deadline

- Stops once the return is filed

Interest compounds daily on both the unpaid tax and the penalty.

Failure-to-Pay Penalty

The failure-to-pay penalty applies when you file but don’t pay the full balance.

- 0.5% per month on unpaid taxes

- Capped at 25%

- Can increase to 1% per month after IRS levy notices

- Reduced to 0.25% per month with an approved payment plan

Combined IRS Penalties

When both penalties apply in the same month:

- Failure-to-file penalty drops to 4.5%

- Failure-to-pay penalty remains 0.5%

- Combined penalty equals 5% per month

IRS Interest Charges

In addition to penalties, the IRS charges interest on unpaid balances.

- Interest compounds daily

- Rate equals the federal short-term rate plus 3%

- For early 2025, the rate is approximately 7%

- Interest is rarely waived

What to Do If You Miss the Tax Filing Deadline

Taking action quickly reduces penalties and interest.

- File your tax return immediately

Stops the failure-to-file penalty from increasing. - Pay as much as you can

Lowers interest and reduces failure-to-pay penalties. - Set up an IRS payment plan

Keeps penalties at reduced rates and prevents aggressive collection. - Request penalty relief if eligible

First-time abatement or reasonable-cause relief may apply. - File for an extension in future years

Form 4868 extends filing—not payment—deadlines.

Special Situations That May Reduce Penalties

Natural Disasters

- Automatic filing and payment extensions

- Penalty relief for federally declared disaster areas

Military Service

- Extended deadlines for active-duty service in combat zones

- Includes filing, payment, and other tax actions

Living Abroad

- Automatic two-month filing extension

- Interest still applies to unpaid balances