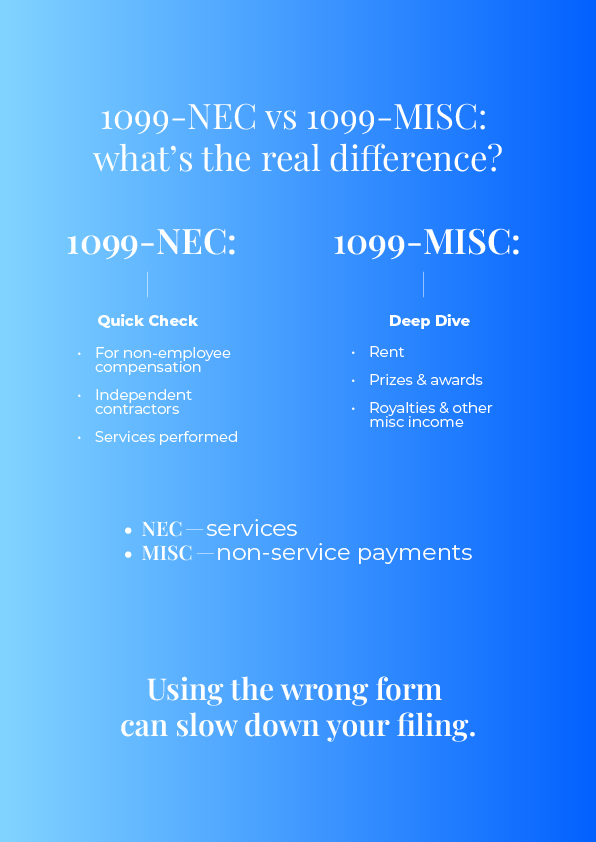

What Is Form 1099-NEC Used For?

Form 1099-NEC is used to report nonemployee compensation. The IRS reinstated this form in 2020 to separate contractor payments from other types of miscellaneous income. Before then, these payments were reported in Box 7 of Form 1099-MISC.

This change made contractor reporting clearer and reduced classification errors.

Who Files Form 1099-NEC?

You must file Form 1099-NEC if you paid $600 or more during the year to a nonemployee for services, including:

- Independent contractors

- Self-employed service providers

- Attorneys providing legal services

- Other nonemployees paid for contract work

The filing deadline is January 31, whether you file electronically or by mail.

What Is Reported on Form 1099-NEC?

- Nonemployee compensation

- Professional service fees

- Cash payments for services

- Contract-based income

- Federal income tax withheld (including backup withholding)

Pros and Cons of Form 1099-NEC

| Pros | Cons |

| Clearly separates contractor income | Tight filing deadline |

| Simplifies IRS tracking | Errors can trigger penalties |

| Easier classification than before 2020 | Requires accurate year-round records |

Form 1099-NEC simplifies contractor reporting, but accuracy and timing matter. Good recordkeeping throughout the year makes filing far less stressful.

How to File Form 1099-NEC

- Obtain official IRS forms (and state copies if required)

- Enter payment and tax information carefully

- File electronically when possible

- Meet the January 31 deadline

- Send Copy B to the contractor

- Retain copies and supporting records

What Is Form 1099-MISC?

Form 1099-MISC reports certain types of payments that don’t qualify as nonemployee compensation. When a payment doesn’t involve services performed by a contractor, this form often applies.

Who Should File Form 1099-MISC?

You must file Form 1099-MISC if you made qualifying payments such as:

- Rent of $600 or more

- Taxable prizes or awards

- Miscellaneous income not reported elsewhere

- Fishing boat crew proceeds

- Certain medical or healthcare payments

What Is Reported on Form 1099-MISC?

| Reportable Payments |

| Rent |

| Royalties |

| Prizes and awards |

| Other taxable income |

| Fishing boat proceeds |

| Medical and healthcare payments |

| Crop insurance proceeds |

| Substitute payments for dividends or tax-exempt interest |

| Gross proceeds paid to attorneys |

| Certain direct sales of consumer goods |

Because this form covers many categories, careful classification is essential.

Pros and Cons of Form 1099-MISC

| Pros | Cons | |

| Covers many payment types | More complex to classify | |

| Useful for non-service payments | Higher risk of reporting errors | |

| Flexible reporting | Requires close attention to IRS rules |

How to File Form 1099-MISC

- Gather recipient and business information

- Obtain the official IRS form or use tax software

- Enter data carefully and double-check amounts

- File electronically when possible

- Mail paper forms only if necessary and retain copies

1099-NEC vs. 1099-MISC: Key Differences

| Feature | 1099-NEC | 1099-MISC |

| Primary purpose | Contractor services | Miscellaneous payments |

| Services reported | Yes | No |

| Rent reported | No | Yes |

| Attorney payments | Services only | Gross proceeds |

| Filing deadline | January 31 | January 31 (most boxes) |

| Introduced | Reinstated in 2020 | Long-standing form |

The IRS separated these forms to reduce confusion and improve reporting accuracy.

Filing Requirements and Compliance

To stay compliant:

- Confirm the correct form before issuing payment

- Collect W-9s early

- Maintain consistent records year-round

- Use accounting software if helpful

- File and distribute copies on time

- Retain documentation for your records

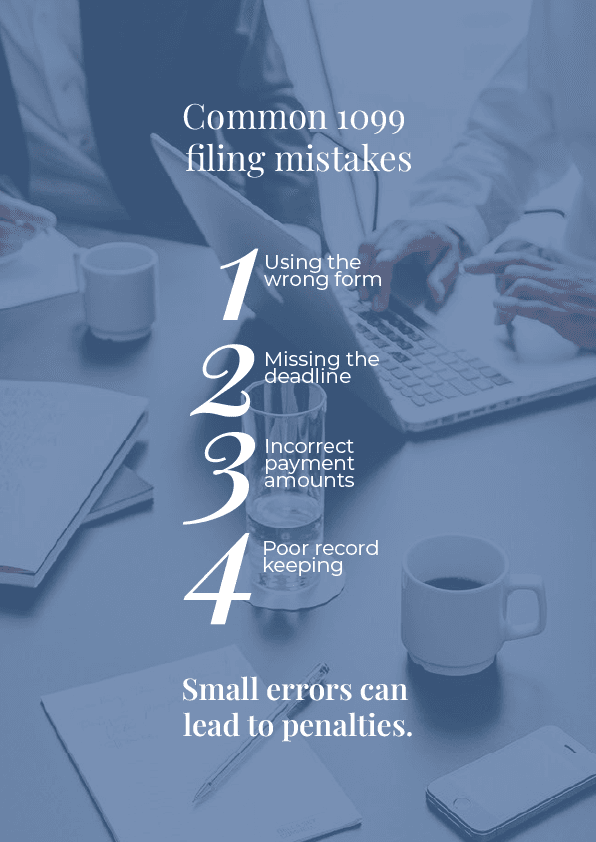

Penalties for Noncompliance

| Timing of Filing | Penalty per Form |

| Filed within 30 days | $50 |

| Filed after 30 days but before August 1 | $100 |

| Filed on or after August 1 | $260 |

Even one missed form can create ongoing issues, especially for small businesses.