What is an Audit?

An audit gives your HOA the highest level of financial confidence within the broader world of audit and assurance. A licensed CPA goes through your records, tests the numbers, and studies your statements to see if they reflect real activity. The work reaches deeper than most people expect. The CPA traces transactions, confirms balances with external evidence, and verifies the flow of money with a level of care that provides your board with a clear picture of your financial position.

Audits usually fall into three groups that serve different needs:

- Internal audit. This looks at your internal controls and daily processes. Boards ask for this when they want to understand how money flows within the community and where potential weak spots might lie.

- External audit. A third-party CPA reviews your statements and your records. This is the type of audit that most financial partners request, as it provides complete independence and the highest level of confidence.

- URS audit. This checks whether your management company follows the required industry standards. Boards often request this during a transition or to confirm that daily work aligns with the expectations set out in the contract.

We see these situations regularly. A new treasurer steps into the role and wants a clean baseline. A board changes management companies and wants outside confirmation that the handover went smoothly. One community told us they felt genuine relief once the CPA walked them through the findings, as it settled months of quiet worry.

Audits cost more and take more time than lighter reviews, but they provide clarity that supports better decisions and stronger trust across the table. This level of detail is why partners often view audits as the strongest form of audit assurance.

What Is Assurance?

Assurance looks at the systems that shape your financial information, which is why assurance in accounting focuses on how your records come together.. Instead of focusing mainly on the final numbers, it studies how those numbers come together. The work extends to the day-to-day activities that support your financial records. It can include controls, staff responsibilities, how your software handles data, and the general flow of information inside the community.

Boards often request assurance to ensure their financial processes work as expected, which is the aim of accounting assurance services. You may have solid statements, but you still want to know that the steps behind those statements hold up under pressure. We typically observe this during leadership changes, shifts in management, or moments when a board senses small inconsistencies and seeks a deeper examination of how things operate behind the scenes.

Assurance helps you understand more than the final result, and this is the core idea behind assurance accounting. It provides a broader perspective and enables you to make more informed decisions by understanding the underlying foundation behind the numbers you rely on.

What Is an Assurance Engagement?

An assurance engagement brings together three key groups in a standard assurance service. Your community provides the information, the assurance CPA performs the work, and the people who rely on your reports use the results to guide their decisions. That audience might include lenders, insurance carriers, bonding companies, or anyone who needs confidence in the strength of your financial process. When all three groups understand their role, the work moves with purpose.

The CPA then studies the subject matter using accepted assurance definition accounting criteria. In most cases, this means your financial records and the systems that support them, but it can also include controls, workflows, and the tools you use to record data. We see boards request this stage when they want more than a surface look at the numbers because they want to understand what drives those numbers day to day.

The next stage involves the criteria that the CPA uses to evaluate the information. These criteria act as the measuring stick. It may be standard accounting guidance or another defined set of expectations that your community must adhere to. With clear criteria, the CPA can identify where your process remains strong and where it needs improvement. One board member told us this was the most helpful part of the engagement because it provided a simple way to understand gaps they had struggled to articulate.

The CPA ends with a conclusion. They report where your systems support accurate information and where risks appear. The purpose is not to accuse anyone. It is to help you understand how dependable your process is, so your board can make decisions with confidence and correct issues before they grow.

Types of Assurance Engagement

Assurance engagements come in two levels. Each level offers a different level of confidence based on the amount of testing the CPA performs.

Reasonable assurance gives your board the strongest comfort. The CPA thoroughly examines your systems, tests specific items, and draws a conclusion based on detailed evidence. Boards choose this level when they want a clear understanding of how well their financial process holds up under closer review.

Limited assurance offers a lighter approach. The CPA still asks questions, reviews your process, and performs targeted checks, but the work does not go as deep as a reasonable engagement. This level works well when your board wants confirmation that the system functions as expected, but does not need the full weight of a higher review.

Both levels help you understand the reliability of your process. The difference comes down to how much clarity you want and how much risk you feel in your current workflow.

Audit vs. Assurance: What Is the Difference?

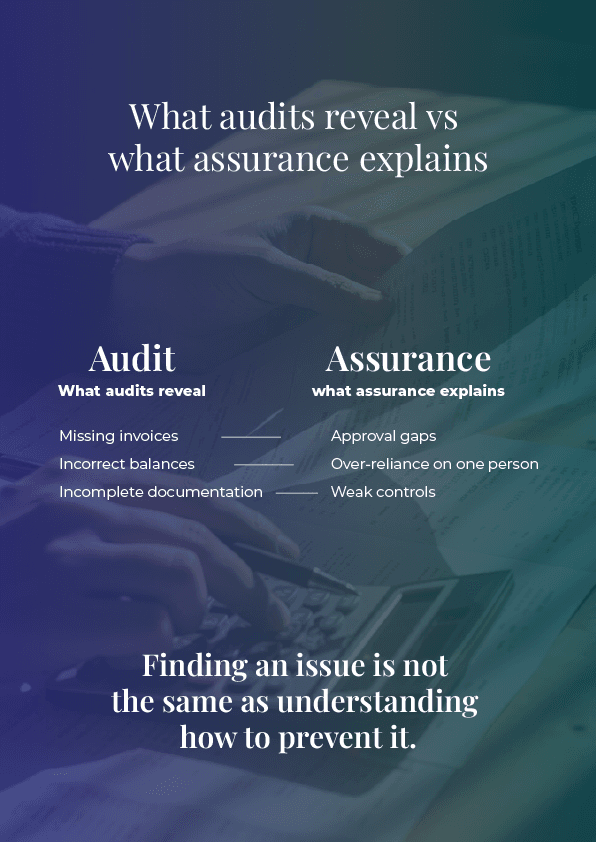

Audits and assurance engagements often overlap, which is why boards sometimes confuse them in discussions about audit vs assurance. An audit is one type of assurance, but its purpose is very specific. The CPA wants to verify that your numbers accurately reflect what actually happened. They test entries, trace transactions, and verify documents until they can confirm that the financial statements accurately reflect the truth. Think of a simple example. Your records may indicate that the community purchased new pool furniture, but the CPA has only found documentation for part of the order. That gap raises a fundamental question. The audit identifies the issue without speculating on the cause.

Assurance steps in when you want to understand the reason behind that gap. The CPA studies the process that produced the records. They look at how your manager collects receipts, how staff approve purchases, and how information moves through your system. One board informed us that their audit revealed several missing invoices. The assurance engagement that followed helped them realize that their approval process relied on a single person, and nothing filled the gap when that person missed a step.

This is the difference that matters for boards when comparing assurance vs audit.. The audit tells you what does not line up. The assurance explains how the issue formed and what part of your process needs support. Together they tell a whole story, but each one answers a different question.

You can think of the contrast in simple terms:

- Purpose. An audit checks accuracy. Assurance checks the strength of the system behind the numbers.

- Focus. Audits follow transactions. Assurance studies workflow and controls.

- Outcome. An audit reveals issues. Assurance helps you understand why those issues appeared and how to prevent them.

Final Thoughts

Audits and assurance engagements serve different purposes, and understanding the distinction helps your board see the difference between audit and assurance. When you understand what each option offers, you avoid guesswork and choose the level of support that fits your community.

SSL Associates helps communities find that balance. We explain your options in plain language, show you what each service covers, and support your board through every step of the engagement.