Form 990: More Than a Tax Filing

Many boards treat Form 990 as a routine federal filing. In reality, it’s a public document that reflects your organization’s governance, financial practices, and credibility.

Form 990 is reviewed by:

- Donors

- Grantmakers

- Journalists

- Watchdog organizations

It communicates:

- How leadership operates

- How funds are used

- Compensation transparency

- Year-over-year financial consistency

A technically correct but incomplete or inconsistent Form 990 can still raise questions. When boards recognize that Form 990 functions as a public profile—not just a tax form—the conversation shifts from compliance to credibility.

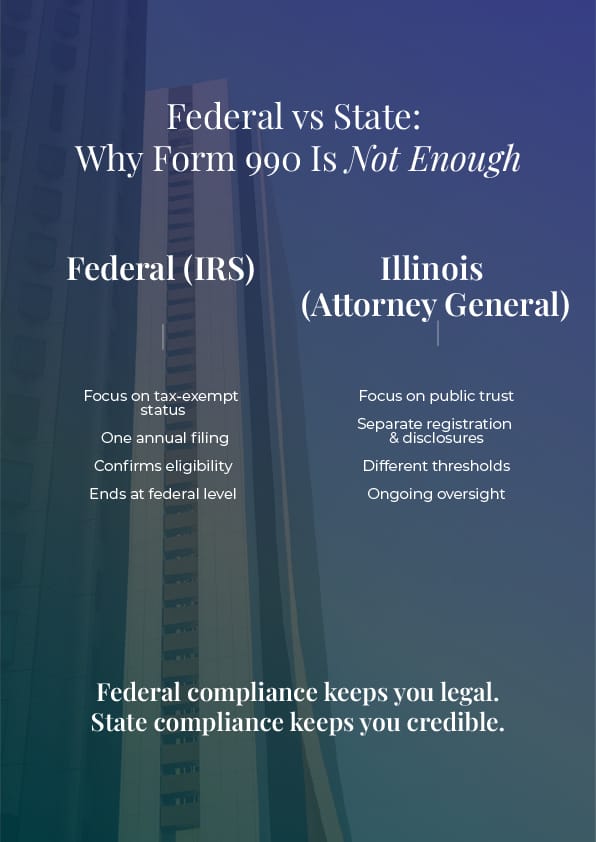

Federal vs. Illinois Oversight

Filing Form 990 with the IRS does not automatically satisfy Illinois requirements.

Federal and state compliance serve different purposes:

| Federal (IRS) | Illinois (Attorney General) |

| Maintains tax-exempt status | Oversees charitable activity |

| Requires annual Form 990 filing | Requires charitable registration & reporting |

| Focuses on tax compliance | Focuses on transparency and public trust |

| Federal deadlines | Separate state deadlines |

Federal compliance keeps your status intact.

State compliance protects public trust.

Illinois Audit vs. Review Requirements

Illinois adjusts financial reporting requirements as nonprofits grow. Revenue thresholds determine whether a nonprofit must submit:

| Organization Size | Required Financial Reporting |

| Smaller nonprofits | No audit or review required |

| Mid-sized nonprofits | Independent financial review |

| Larger nonprofits | Full independent audit |

Crossing a revenue threshold can trigger higher reporting standards—often without obvious notice.

Growth is positive, but it changes expectations.

Audit vs. Review: What’s the Difference?

An audit and a review are not interchangeable.

| Audit | Review |

| Extensive testing and verification | Limited analytical procedures |

| Formal opinion issued | Limited assurance provided |

| Higher level of scrutiny | Focuses on reasonableness |

| Required for larger nonprofits | Required for mid-sized nonprofits |

Submitting the wrong level of financial report can delay filings and create unnecessary follow-up with the Illinois Attorney General’s office.

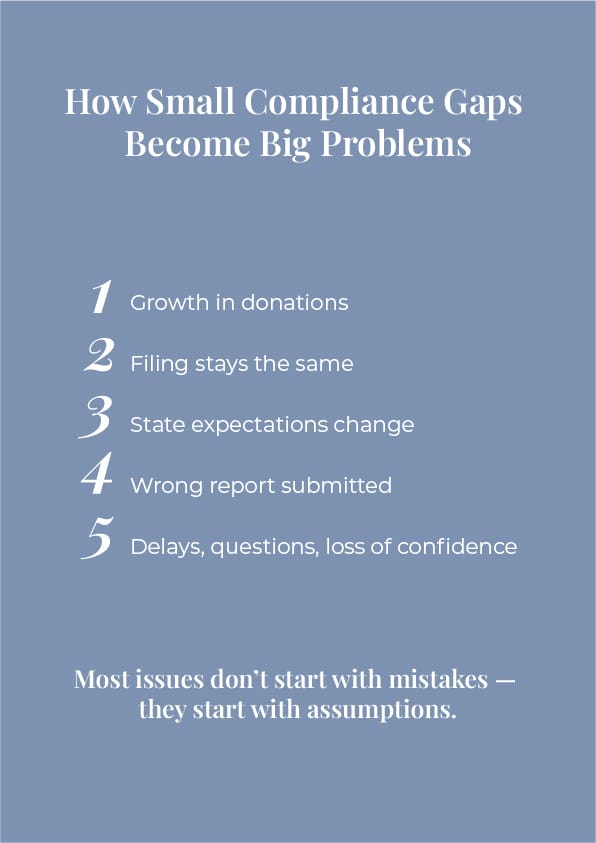

Where Illinois Nonprofits Commonly Run Into Trouble

Most compliance issues do not start with wrongdoing. They begin with assumptions.

Common challenges include:

- Filing Form 990 but overlooking Illinois charitable registration

- Continuing last year’s reporting structure despite revenue growth

- Missing state-specific deadlines

- Assigning compliance to one person instead of board oversight

- Waiting until questions arise before reviewing filings

Federal and state deadlines are separate—and not always aligned.

Staying Ahead of Compliance

When nonprofit growth aligns with updated compliance practices:

- Filings reflect your current size and activity

- Audit or review requirements are properly met

- State registrations remain current

- Board leadership stays informed

Compliance should evolve alongside growth—not trail behind it.