Why Weak Internal Controls Develop in Nonprofits

Internal control gaps usually grow from practical decisions, not negligence.

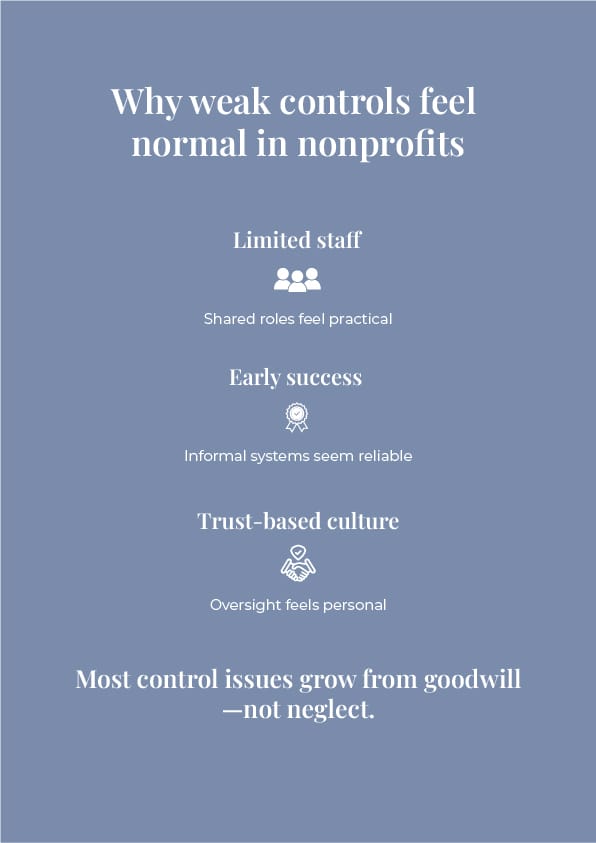

Common contributing factors include:

- Limited staff handling multiple financial roles

- Informal approval processes

- Lack of documented procedures

- Board oversight focused only on summary reports

In small organizations, combining duties may feel efficient. As revenue and operations expand, those same structures increase fraud risk and error exposure.

What Are Internal Controls in a Nonprofit?

Internal controls are policies and procedures that:

- Protect cash and assets

- Ensure accurate financial reporting

- Prevent and detect fraud

- Support board oversight

They are not about distrust. They are about accountability and clarity.

When one person approves expenses, records transactions, and reconciles bank statements, segregation of duties is missing. That structure increases both fraud risk and audit exposure.

Common Internal Control Weaknesses in Nonprofits

Weak nonprofit internal controls often include:

- One individual handling cash, recording transactions, and performing reconciliations

- Infrequent bank statement review

- Undocumented expense approvals

- Limited board review of financial details

- Inconsistent documentation of reimbursements

These gaps create opportunities for:

- Unintentional errors

- Misstated financial reports

- Fraud that goes undetected

Even small control weaknesses can lead to larger reputational damage.

How Weak Controls Increase Fraud Risk

Fraud risk increases when three conditions exist:

- Opportunity (lack of oversight or segregation of duties)

- Pressure (financial or organizational stress)

- Rationalization (“No one will notice”)

Weak internal controls primarily increase opportunity.

Nonprofits often operate in trust-based cultures. While trust is essential, it cannot replace structure. Strong internal controls protect both the organization and its staff.

The Board’s Role in Nonprofit Internal Controls

Board members have fiduciary responsibility for oversight, even if they are not involved in daily accounting.

Effective board oversight includes:

- Reviewing detailed financial reports

- Ensuring segregation of duties where possible

- Asking questions about reconciliation processes

- Confirming documented approval policies

- Engaging in periodic internal control reviews

Waiting until an audit uncovers a weakness increases cost and stress.

Proactive oversight prevents reactive corrections.

What Happens When Controls Break Down

When internal controls fail, consequences can include:

- Audit findings

- Financial restatements

- Donor concerns

- Leadership distraction

- Reputational harm

Even when the financial impact is small, public trust can suffer significantly.

The cost of rebuilding systems and credibility often exceeds the cost of implementing preventive controls early.

Strengthening Nonprofit Internal Controls

Nonprofits can reduce fraud risk and improve financial clarity by:

- Separating financial duties when possible

- Implementing documented approval workflows

- Conducting regular bank reconciliations with independent review

- Formalizing reimbursement and expense policies

- Performing periodic internal control assessments

Internal controls are not a constraint on mission work. They are a foundation for sustainable growth.

Protect Your Nonprofit from Fraud and Control Gaps

Strong nonprofit internal controls support:

- Accurate financial reporting

- Board confidence

- Audit readiness

- Donor trust

- Long-term stability

SSL Associates works with nonprofits to assess internal controls, identify fraud risk areas, and implement practical safeguards that align with staffing realities.

If you are unsure whether your nonprofit’s internal controls are strong enough, a proactive review can provide clarity before problems surface.